Based on CSRD, certain company categories must proceed with the mapping of their activities with the EU Taxonomy in their annual reports. We support our clients (either larger companies under the CSRD or financial institutions) identify the portion of their activities that constitute Taxonomy-eligible, Taxonomy-non-eligible and Taxonomy-aligned activities in terms of their Turnover, CAPEX and OPEX, respectively.

Under the CSRD companies map their activities using the EU Taxonomy in their annual reports.

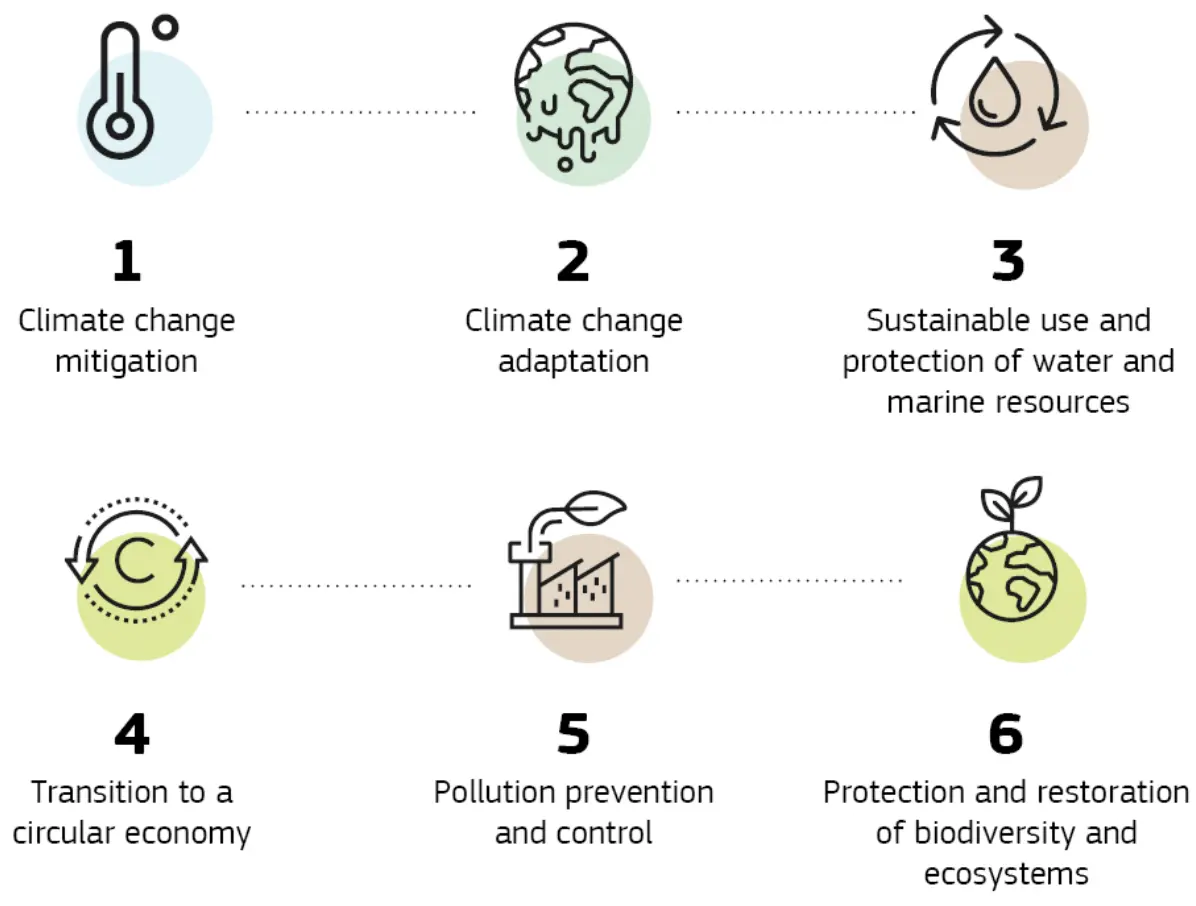

EU Taxonomy is a standardized way to categorize eco-friendly economic activities, and for financial institutions to support sustainable investments

EU Taxonomy - Mandatory Disclosures

Applicable to larger companies under the CSRD.

EU Taxonomy Methodology

Determine Eligibility:

Assess whether there is a description and TSC within the EU Taxonomy navigator or Annex I & II of the Climate Delegate Act for an activity.