The Corporate Sustainability Reporting Directive (2022/2464/EU) is a regulatory framework implemented to enhance sustainability reporting by companies in the EU.

The directive was adopted by the European Commission on November 2022, and entered into force on January 2023. In 2025, adjustments to scope and timelines were introduced via the ‘Omnibus’ package.

In 2025, the EU introduced the Omnibus “Stop the Clock” Directive and Quick-Fix delegated act, postponing reporting deadlines for certain companies by up to two years and simplifying technical requirements for first-wave entities.

The CSRD aims to expand the scope of reporting requirements beyond financial performance to include environmental, social, and governance (ESG) factors and make sustainability reporting more consistent, transparent, and reliable across the EU.

Corporate Sustainability Reporting Directive

The CSRD applies to various types of companies, including large, small, and medium public-interest entities (PIEs). These include:

Listed companies on regulated markets.

Credit institutions, insurance companies, and cooperatives.

Large non-listed EU companies, which are now also required to report under CSRD.

Non-EU companies generating significant turnover in the EU (≥ EUR 150 million) with a large or listed EU subsidiary or branch.

Who needs to comply with the CSRD and when?

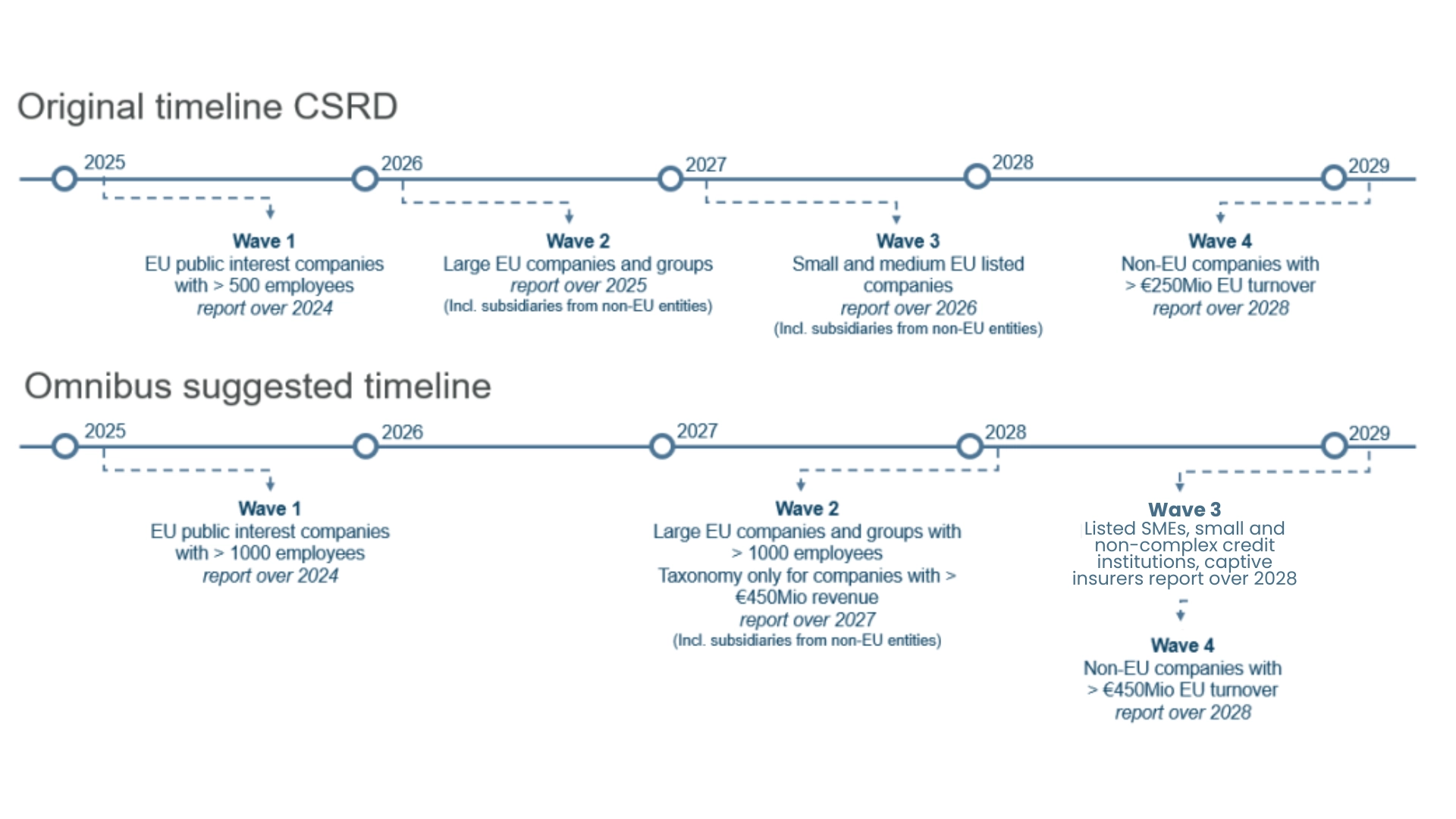

Due to the Omnibus package, the reporting deadlines for some categories have been postponed by two years:

Large PIEs already subject to NFRD → still report first, for FY 2024 (Wave 1 – reports in 2025).

Other large companies → originally FY 2025, now postponed to FY 2027 (Wave 2 – reports in 2028).

Listed SMEs, small and non-complex credit institutions, captive insurers → originally FY 2027, now postponed to FY 2028 (Wave 3 – reports in 2029).

Non-EU companies with EU turnover ≥ EUR 150 million → FY 2028 (Wave 4

– reports in 2029).

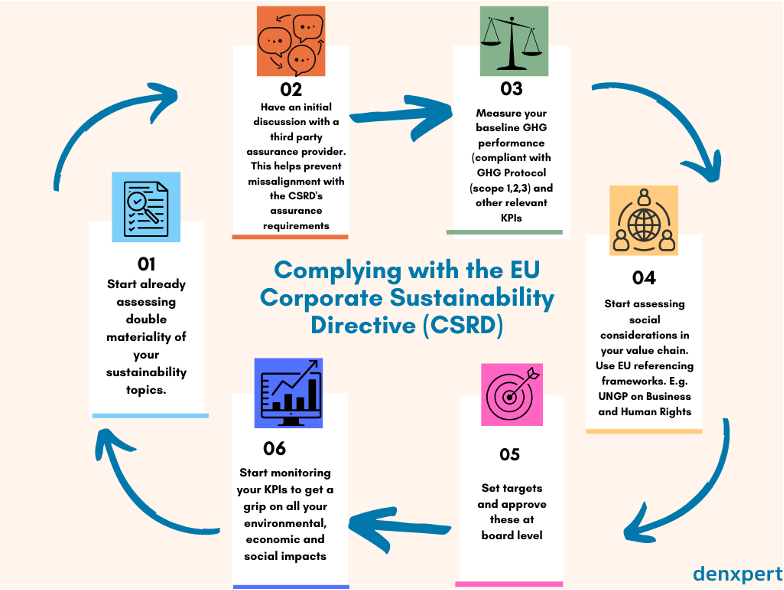

Assess current reporting practices and enhance non-financial data collection and management.

Collaborate with and engage stakeholders to identify material sustainability issues and improve reporting relevance and transparency.

Develop a roadmap and allocate resources to prepare for compliance with CSRD obligations, including training staff and integrating sustainability into business strategy and operations.

How to report in accordance with the CSRD?

The CSRD aligns reporting requirements with the European Sustainability Reporting Standards (ESRS), ensuring consistency and comparability in sustainability reporting across the EU.

The ESRS represents a major shift, creating new demanding transparency obligations on companies regarding their commitment to sustainability and providing a framework for reporting on ESG topics.

It applies to companies within the scope of the CSRD, with first-time application starting from FY 2024 (reporting in 2025).

Disclaimer

This update is for information purposes only and is not intended to constitute legal advice or be a substitute of the detailed provisions of applicable laws.