Your Partner on your ESG transformation journey

Environmental risks are becoming systemic and a potential threat to financial stability. We diagnose the relationship between banking regulation and environmental challenges, including climate change, and consider what regulatory and policy enhancements are necessary to enable a transition to a more sustainable economy. We contribute to managing the financial stability risks associated with environmental challenges and fortify the Bank’s green transition.

Having adopted TCFD principles, we provide organizations as well as prospective investors with the relevant information to understand their opportunities and risks (physical & transitional) associated with climate change in a market.

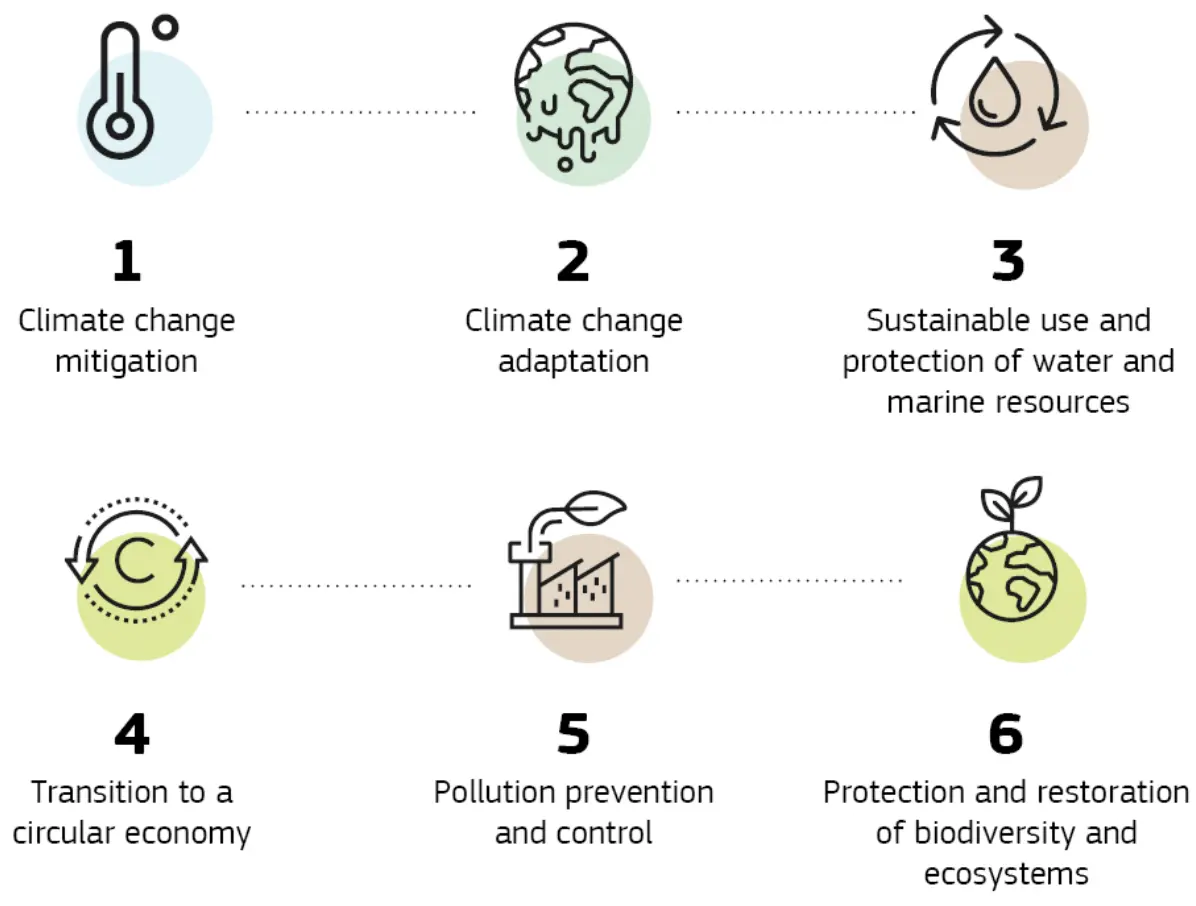

In a world facing the triple planetary crises of climate change, biodiversity loss, and pollution, sustainability has never been more critical for firms and communities. In late June 2023, the Financial Stability Board announced that the work of the TCFD has been completed and replaced by the two ISSB standards, IFRS S1 and IFRS S2, which officially came into effect at the start of 2024. NZA team is well-positioned to help companies/clients apply IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures, covering TCFD recommendations as the latter are fully incorporated into the ISSB’s Standards.

The European Banking Authority (EBA) published on 13th December 2022 its roadmap outlining the objectives and timeline for delivering mandates and tasks in the area of sustainable finance and environmental, social, and governance (ESG) risks

Based on the guidelines, the institutions will be required to include the ESG factors in their risk management policies, including credit risk policies and procedures. The guidelines also set out the expectation that institutions that provide green lending should develop specific sustainable finance policies and procedures covering granting and monitoring of such credit facilities. These guidelines are the first specific policy product developed by the EBA incorporating sustainability considerations.

Incorporating ESG into the overall Governance Organizational Model and Risk Management framework

Integrating of ESG risks into the Risk Appetite Framework

Incorporating ESG factors in the loan origination and monitoring process

Estimation of financed emissions, including Scope 3

Performing the Materiality Assessment of ESG risks

Development of the climate change stress testing capacity.

Incorporating ESG into Business strategy.

Drafting and implementing a sustainable financing framework.

Development of internal and external (Disclosures) Reporting framework

ΝΖΑ, being a subject-matter expert, assists banks in setting basic practices in place for most of the ECB’s expectations, including: mapping of climate-related and environmental risk exposures, allocating responsibilities, selecting and reporting KPIs and KRIs and finally developing effective mitigation strategies. Being aware of the forward-looking approaches needed to manage climate and environmental risks, our team highly contributes in developing advanced strategies to embedding climate and environmental risks into client due diligence and lending policies.

In a world facing the triple planetary crises of climate change, biodiversity loss, and pollution, sustainability has never been more critical for firms and communities. In late June 2023, the Financial Stability Board announced that the work of the TCFD has been completed and replaced by the two ISSB standards, IFRS S1 and IFRS S2, which officially came into effect at the start of 2024. NZA team is well-positioned to help companies/clients apply IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures, covering TCFD recommendations as the latter are fully incorporated into the ISSB’s Standards.

Based on CSRD, certain company categories must proceed with the mapping of their activities with the EU Taxonomy in their annual reports. We support our clients (either larger companies under the CSRD or financial institutions) identify the portion of their activities that constitute Taxonomy-eligible, Taxonomy-non-eligible and Taxonomy-aligned activities in terms of their Turnover, CAPEX and OPEX, respectively.

In January 2024, EU banks will have to disclose their Green Asset Ratio (GAR) for the financial year 2023. This means that banks will need to provide quantifiable evidence that demonstrates the extent to which the activities they finance meet what the EU Taxonomy defines as sustainable.

In general, the climate risks on banks’ balance sheets and the effectiveness of their transition plans will affect stakeholders’ assessments of the banks’ business strategy and financial resilience, potentially affecting their share price or credit rating, and in turn access to and cost of capital and funding. As a summary measure of greenness, the GAR could in turn be adopted as a key determinant in the assessments by equity and debt investors. Investors may rely on banks’ GARs to identify green finance leaders and laggards, and a low outlier could serve as a red flag against a bank’s ESG characteristics.

Adding {{itemName}} to cart

Added {{itemName}} to cart